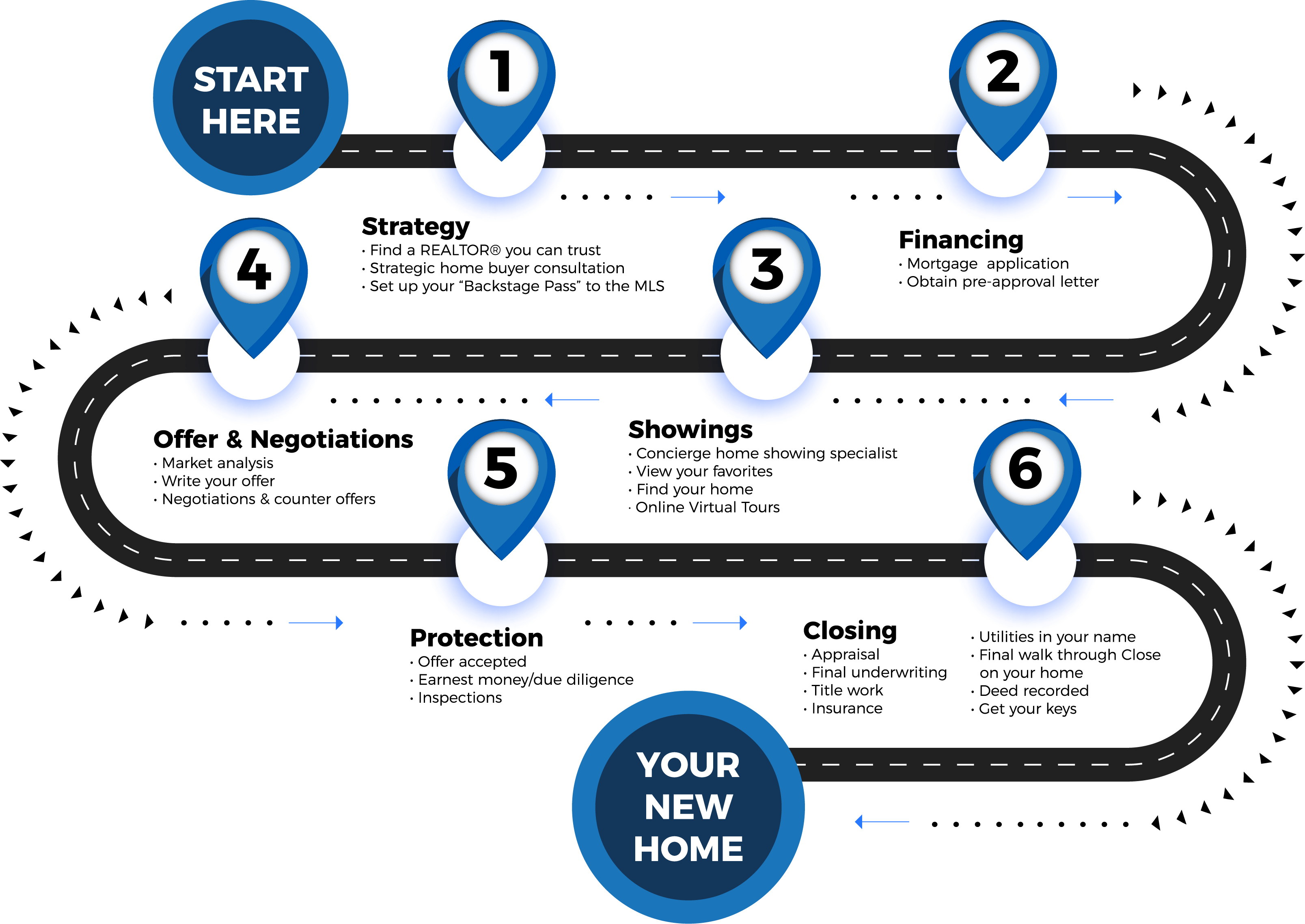

Buying a home is an exciting journey, but it’s also one that requires preparation and planning. One of the most critical steps in this journey is getting pre-approved for a mortgage. This step not only clarifies your budget but also shows sellers you’re serious about making an offer. Let’s break down what the pre-approval process entails and why it’s so important.

What Is a Mortgage Pre-Approval?

A mortgage pre-approval is a lender’s conditional offer to loan you a specific amount of money based on your financial situation. It’s not a guarantee of a loan, but it’s a strong indicator of how much house you can afford and the terms you might expect. A pre-approval is more comprehensive than pre-qualification, as it involves a detailed review of your financial information.

Why Is Pre-Approval Important?

- Clarity on Budget: Pre-approval gives you a clear understanding of your price range, saving you time by focusing on homes within your financial reach.

- Stronger Offers: Sellers and real estate agents often take pre-approved buyers more seriously, as it shows you’re financially prepared.

- Faster Closing Process: With much of the financial review already completed, a pre-approved buyer can often close on a home more quickly.

Steps to Get Pre-Approved

- Gather Financial Documents: Lenders will require documents such as:

- Proof of income (e.g., pay stubs, tax returns, W-2s or 1099s)

- Proof of assets (e.g., bank statements, investment accounts)

- Credit history

- Identification (e.g., driver’s license, Social Security number)

- Check Your Credit Score: Your credit score plays a significant role in determining your loan eligibility and interest rate. Before applying, review your credit report for errors and work on improving your score if needed.

- Choose a Lender: Research and compare lenders to find one that offers favorable terms. Consider factors like interest rates, customer reviews, and responsiveness.

- Submit an Application: Fill out the lender’s application form, providing accurate and complete information. This will include details about your income, debts, and employment history.

- Undergo a Credit Check: The lender will perform a hard inquiry on your credit report to assess your financial health.

- Receive Your Pre-Approval Letter: If approved, you’ll receive a pre-approval letter stating the loan amount, interest rate, and loan terms. This letter is typically valid for 60 to 90 days.

Tips for a Smooth Pre-Approval Process

- Be Honest: Providing accurate information helps avoid delays or denials.

- Avoid Major Purchases: Large purchases or taking on new debt can negatively impact your credit and pre-approval status.

- Stay Organized: Keep your financial documents up to date and easily accessible.

The pre-approval process might seem daunting, but it’s a crucial step in becoming a confident and prepared homebuyer. By securing pre-approval, you’ll not only streamline your home search but also position yourself as a serious contender in a competitive market. So, take the time to get pre-approved and start your home buying journey on solid financial footing.

{kind=link}

{kind=link}